Why the Biden administration’s infrastructure plan could spark a decade-long supercycle for building materials, spilling over to the rest of the U.S. economy. 6 takeaways for investors.

After decades of underinvestment, U.S. roads, bridges, ports, airports and transit systems could be closer to their own shot in the arm, with the introduction of the Biden administration’s ambitious infrastructure package.

Despite the greater focus on elements related to clean energy and electric vehicles, the old-fashioned infrastructure and building materials—think concrete and asphalt roads, steel for bridges—could deliver an outsized economic impact.

“An infrastructure package could catapult building materials into a supercycle similar to the 1950s," says Morgan Stanley Equity Analyst Nikolaj Lippmann. “We are 10 years into the current construction cycle, exiting a recession, and potentially facing a government-underwritten cycle of another 10 years."

In a series of related reports, Lippmann and his colleagues examine which types of structures need repair, who could directly benefit and how this might spill over to the rest of the economy. Here are six takeaways from their analysis of the core infrastructure package.

1. CORE INFRASTRUCTURE HAS A HIGH PROBABILITY OF PASSING

The infrastructure package, currently one of four major categories outlined in the American Jobs Plan (AJP), includes investing in: traditional infrastructure, environmental infrastructure, technology research and development, and social programs.

Many hurdles remain for the deal to get done before the end of third quarter; however, Congress currently seems highly inclined to make progress on traditional infrastructure. “As it stands today, we believe an infrastructure plan, at levels close to the Moving Forward Act, is more likely," says Michael Zezas, Head of U.S. Public Policy Research, referring to the 2020 House bill that stalled in the Senate. That bill targeted fixing existing infrastructure before constructing new roads and bridges, with more immediate impact on local economies.

Investors should also keep their eye on the Supreme Court case California v. Texas as a potential spoiler to early passage of an infrastructure bill. The case will decide the constitutionality of the Affordable Care Act. “In our view, if the ACA were struck down by the Supreme Court, it could create a catalyst for Congress to act on health-care legislation in the place of infrastructure," notes Zezas.

2. A NEW SUPERCYCLE AHEAD

If passed, a core infrastructure package could drive demand for building materials, including cement, aggregates (sand, gravel) and possibly steel, and boost the revenues of manufacturers. Led by major investment in concrete, heightened demand would outstrip production capacity and drive higher pricing.

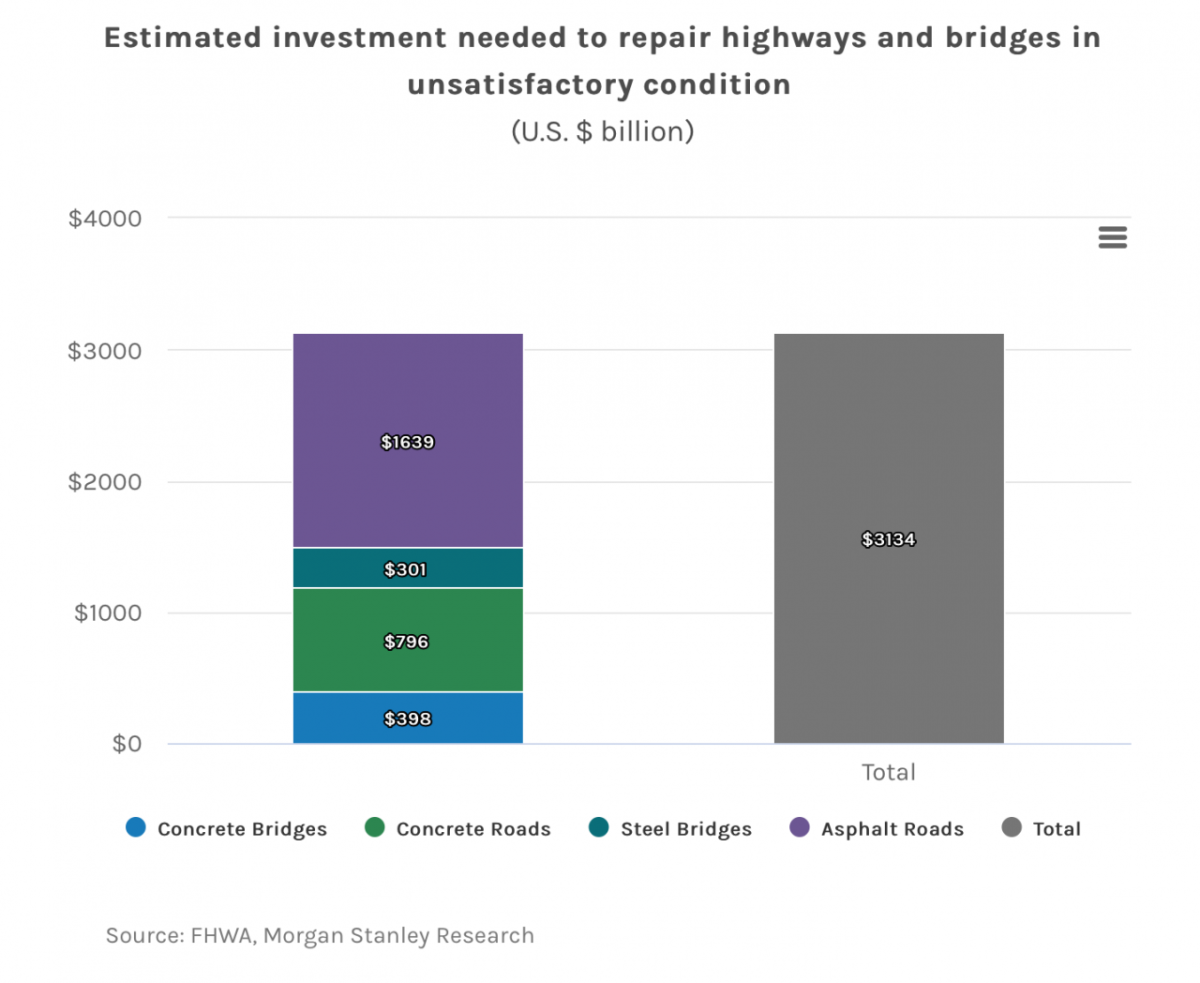

Work conducted by AlphaWise, the proprietary survey and data arm of Morgan Stanley Research, mapped $3 trillion in needed infrastructure repairs along with companies that could provide them. Needed repairs break down to about $398 billion for concrete bridges, $796 billion on concrete roads, $300 billion for steel bridges and $1.6 trillion to upgrade asphalt roads.

3. CEMENT PROFITABILITY COULD DOUBLE

The single biggest beneficiary of a traditional infrastructure package is cement. “With the U.S. cement industry at 90% production capacity 30% import capacity, prices would be pressured materially higher," says Carlos De Alba, equity analyst and head of Morgan Stanley's Americas Basic Materials research team.

De Alba estimates that a 15% to 20% real price increase could double U.S. cement earnings over the next five years. Because of the lack of suitable substitutes, cement is a highly inelastic product. “We estimate cement could reach $70 to $85 per ton on the low end. And as domestic cement supply approaches capacity, the industry will increasingly need to import cement, which ultimately could mean greater profit margins for domestic producers.”

Infrastructure spending would also require about nine billion metric tons of aggregates—or the equivalent of about four years of demand—with highway resurfacing driving the largest demand.

4. STEEL ALSO STANDS TO BENEFIT

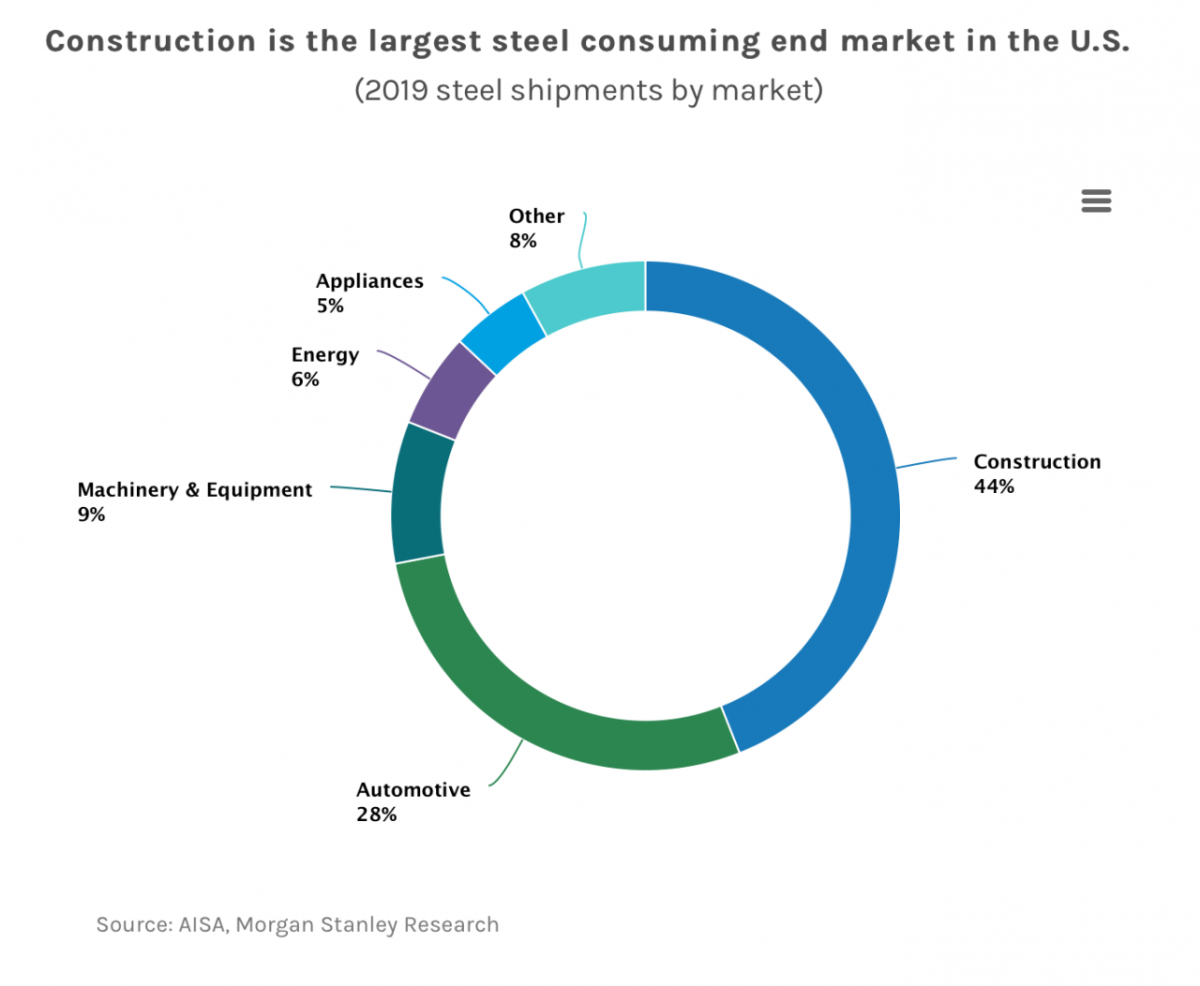

Construction is one of the largest end-markets for finished steel products in the U.S., accounting for nearly 44% of annual domestic steel shipments.

Industry sources estimate that every $1 billion dollars spent in infrastructure translates to approximately 50 kilotons of steel demand. Using this rough estimate, a $1.5 trillion/10-year infrastructure plan would translate to 75 metric tons of incremental steel demand over 10 years. Although rebar could benefit the most, thanks to strong cement consumption, demand for steel will ultimately depend on the type of projects included in the final infrastructure package. For example, wind turbine towers use about 200 tons of steel per tower, and electrical grids use 30 to 35 tons per mile.

5. CONSTRUCTION STOCKS COULD RERATE

Infrastructure spending bodes well for domestic construction stocks across the board. “When the construction industry is underwritten by the federal government, it lowers investment risk and gives industries pricing power, improving profitability and the risk-reward profile for construction materials," says Lippmann. Moreover, the infrastructure program will likely emphasize repairs over new infrastructure, providing a higher return on investment.

Looking at the stock-rerating patterns of domestic construction names around past key infrastructure events, on average, most stock gains, in terms of expanded price-to-earnings multiples, occur by the third month after bill passage.

6. INFRASTRUCTURE’S MULTIPLIER EFFECT

The infrastructure package would likely ripple well beyond building products. In fact, Morgan Stanley economists see widescale productivity benefits from a large infrastructure package. A $1 trillion,10-year package could add 0.2 percentage point to GDP in subsequent years and 715,000 jobs over 10 years. “Add to this the potential boost from fiscal stimulus and it could add as much as 0.4 to 0.8 percentage point to annual GDP growth rates," says Ellen Zentner, Morgan Stanley Chief U.S. Economist.

Zentner adds that the increased public investment in infrastructure could provide even longer-term tailwinds for the U.S. economy. “The current body of literature on government multipliers finds that infrastructure spending policies carry multipliers as high as two times. In other words, each fiscal dollar increases gross output by two dollars."

For more Morgan Stanley Research on U.S. infrastructure spending ask your Morgan Stanley representative or Financial Advisor for the full report, “Paving the Way for a U.S. Infrastructure Super Cycle." Plus, more Ideas from Morgan Stanley's thought leaders.