Our latest Horizons: Alternative Proteins report reveals significant growth in the industry, with cultivated meat and fermentation-derived proteins producers making the most notable leaps. However, manufacturers are still facing obstacles around scale-up, sustainability, and regulatory approvals.

I find myself particularly impressed by today’s manufacturers of alternative proteins. They’re relatively new to the scene, they’re competing in an unproven marketplace, and they face regulatory and commercial challenges that the traditional food and beverage industry can’t necessarily solve for them. Despite all of this, they’re persisting—thriving, even. The 2023 Horizons: Alternative Proteins report, based on detailed survey responses from more than 150 manufacturers in operation today, is proof.

When we last surveyed this industry in 2021, we found both optimism and uncertainty among manufacturers, often in equal measure. Test kitchens were generating innovative products and processes, but the challenges of commercial scale-up were frustrating even for the most well-established operators.

Two years later, our updated survey charts a promising evolution:

- More than 70% of survey respondents are manufacturing at commercial scale, up from 65% in 2021—a signal that manufacturers are solving at least some of their scalability challenges.

- 66% of respondents have seen an increase in sales volume since 2021—a signal that consumer demand for alternative proteins is healthy and growing.

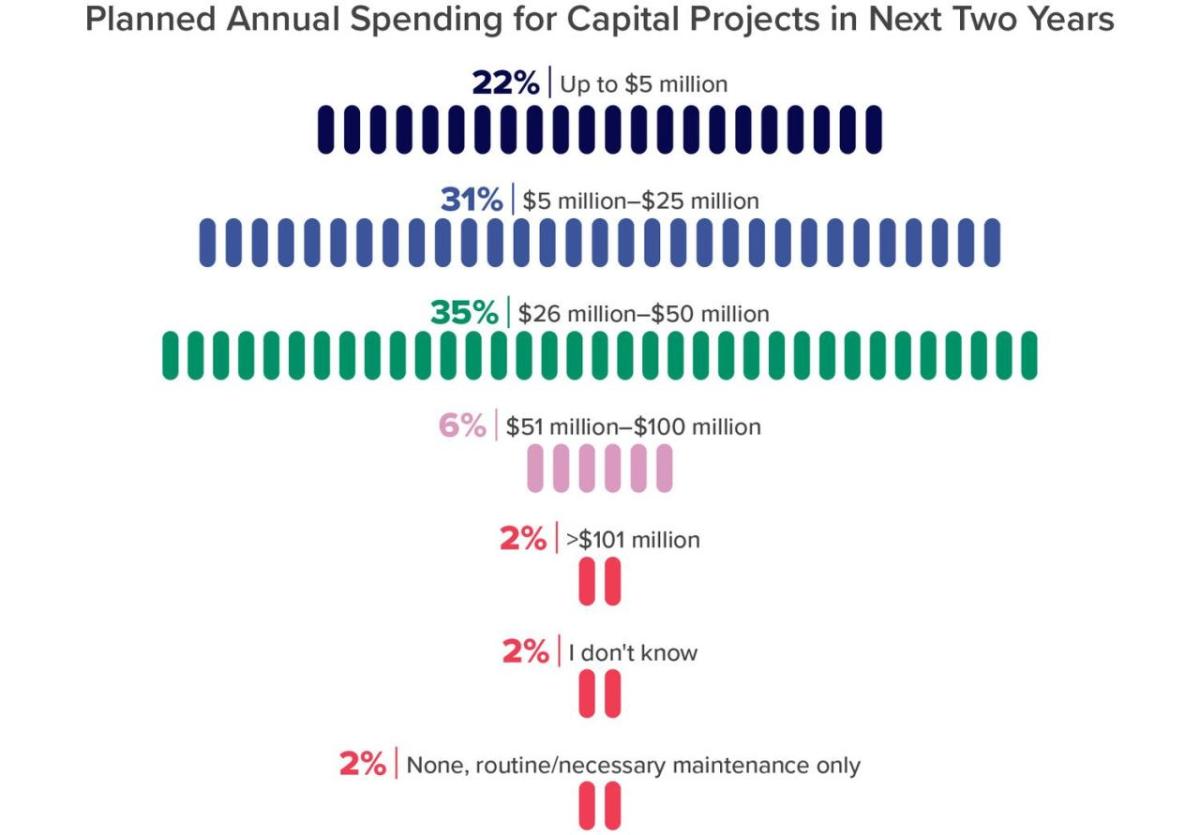

- Today’s manufacturers plan to spend nearly 50% less on capital projects than they did in 2021—a signal that manufacturers are more strategic with their budgets, investing surgically where capital is needed and benefiting from their early investments in flexible, future-proof facilities designed to sustain long-term growth.

What does “alternative protein” mean?

The term “alternative proteins” refers to meats and dairy products that may be plant-based or produced through cell cultivation or fermentation.

More interesting is what hasn’t changed. Average company sizes remain largely consistent between 2021 and 2023; then as now, only about a third of respondents have more than 1,000 employees. This could indicate a healthy pipeline of new and pioneering entrants, but it’s also a signal of persistent challenges—consider the large-scale layoffs, high-profile recalls, and bleak outlooks from market analysts that have recently plagued this industry. It does not appear the industry has seen large-scale consolidation, as some had predicted. How can these manufacturers maintain the resilience and ingenuity that got them this far in the face of such formidable challenges? In this report, we will attempt to answer questions like this one by examining our survey data through a series of lenses, including:

Cultivated Meat

Our survey responses highlight the maturation of the cultivated meat industry. Price parity is coming soon, at least for premium or value-added products, and most manufacturers are hopeful that their products will be on the market within two years. But to achieve this—while making a profit—production levels must rise and costs must fall.

Join Derek Ung, Sebastian Bohn, and Krizia Diaz as they unpack this challenge and deliver good news: There has been an exponential decrease in the cost of culture media, by far the most expensive material two years ago, and production targets have risen dramatically since our last report. Momentum is certainly in the right direction, and if the challenges identified by our trio of experts are addressed, the outlook for a sustainable and profitable future is good.

Fermentation Derived Proteins

A surprise awaited Sebastian Bohn, Brendan Kress, and Tony Moses when they examined the survey data from this segment. They had expected fermentation-derived proteins manufacturers to overtake cultivated meat manufacturers in terms of go-to-market readiness—what they didn’t expect was to see these manufacturers move ahead of all other markets and emerge as the most commercially advanced segment in our survey.

However, the path ahead may not be smooth. Our survey data reveals a few challenges brewing that will soon boil over. For example, respondents in this segment are hoping that a sustainability-focused promise will justify a premium price, despite acknowledging, in a different survey question, that sustainability isn’t driving consumers’ buying behavior in a significant way. To continue their successful trajectory, manufacturers in this segment will need to address these problematic areas—and soon.

Plant- and Mycelium-based Meat

Given the grim headlines hounding plant-based protein manufacturers, our experts Jason Tucker and Tony Moses wondered if the survey results would uncover a slump in growth. However, they discovered a surprisingly robust pipeline of new entrants, and an interesting pivot in terms of this segment’s core identity: Instead of nobly setting forth to save the planet, today’s plant- and mycelium-based manufacturers have developed a savvy business model that’s hardly discernable from the mature commercial strategies guiding today’s traditional food and beverage industry.

How can manufacturers in this segment continue this trend toward resilient business practices and reliable growth? In this section, Tucker and Moses dive into the survey data to propose an answer.

Plant-based Dairy

A subtle but remarkable shift is underway in the plant-based dairy segment. Two years ago, our survey respondents indicated a keen focus on upstream innovation as they searched for the right ingredients and formulations to offset their material costs while perfecting their core offering. As our experts Pablo Coronel and Jonathan Clark note, today’s producers have the same appetite for innovation, but it’s playing out further downstream.

Packaging upgrades hover near the top of manufacturers’ capital investment wish list. As well, diverse formats like cheese, sour cream, and yogurt are catching up to—and in some cases surpassing— fluid milk alternatives in the overall product pipeline. To keep this momentum going, our experts advise an optimistic but measured approach to future development—more haste, less speed.

Sustainability

Most alternative protein manufacturers indicate that they have sustainability budgets, while fewer have goals and concrete plans to put those budgets to work. In this section of our report, experts Maya DeHart, Aaron Kilstofte, and Jonathan Dressler go deep into the survey data to understand and contextualize this phenomenon, and to offer advice for companies trying to access the rewards of good environmental stewardship from both a brand positioning perspective and in terms of ROI and optimized manufacturing.

Their key advice? Get started now and develop a strategy that will steer you away from a troubling pattern noted in the survey data—that is, a growing disconnect between capital expense planning and the complexity of making meaningful changes at a facility level to achieve sustainability goals.

Regulations

As companies mature from start-up to production scale, the importance of food safety and hygiene is clearly

paramount. Our respondents indicate an improved understanding of the regulations that govern them and have dedicated significant resources to quality assurance, compliance, operational procedures,

and facility upgrades.

How does this evolution in regulatory maturity play out across companies of different sizes? Join experts Dennis Collins and Pablo Coronel as they offer their perspectives on what companies at both ends of the CapEx spectrum are doing to implement a strong regulatory strategy—and, more importantly, to earn and maintain the trust of consumers.

Alternative protein manufacturers need a strong commercial strategy

To operate successfully at a commercial scale, manufacturers of alternative proteins need a strategy that integrates both consumer expectations and the realities of operating a large-scale food and beverage plant.

This is, perhaps, our biggest takeaway from the 2023 survey: to shift from a fledgling idea to a cash-positive manufacturing company, today’s manufacturers of alternative proteins are pushing themselves beyond the single-note mission that may have galvanized them initially (“Let’s change the world!”) and toward a savvier, more nuanced commercial strategy (“Let’s generate a sustainable profit by selling cost-effective products!”). This shift may not inspire powerful feelings in the heart, but it does generate a powerful balance sheet. It’s this industry’s best hope for continued progress in an increasingly wild world.

To access more insights on the life sciences manufacturing industry, download the report below.