by Michal Grinstein-Weiss and Salah Goss

Small business owners have faced unequal financial challenges during the pandemic. We have all heard the anecdotes about the store owner who dipped into their personal savings to cover emergency costs or payroll. Sure, support arrived from Washington for some, yet it was often neither sufficient nor easily accessible.

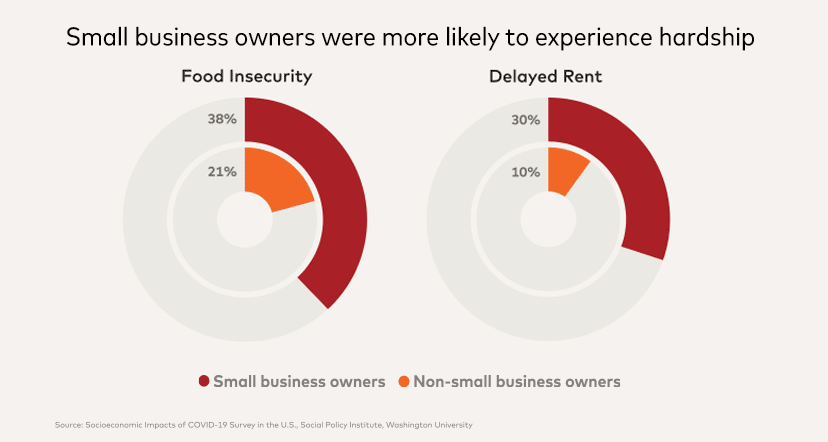

New data is starting to shed fresh light on some of the dramatic disparities and difficulties facing this engine of the American economy. Research out of the Social Policy Institute at Washington University in. St. Louis found that small business owners were in fact two to three times more likely to have a personal financial hardship in the last two years. Not only did the personal savings of these households plummet, many were unable to pay basic bills and often faced food shortages.

And there was one particularly stark statistic that stood out from the data: small business owners were two to three times as likely to experience income losses or hardships like skipped housing payments and food insecurity than non-business owners.

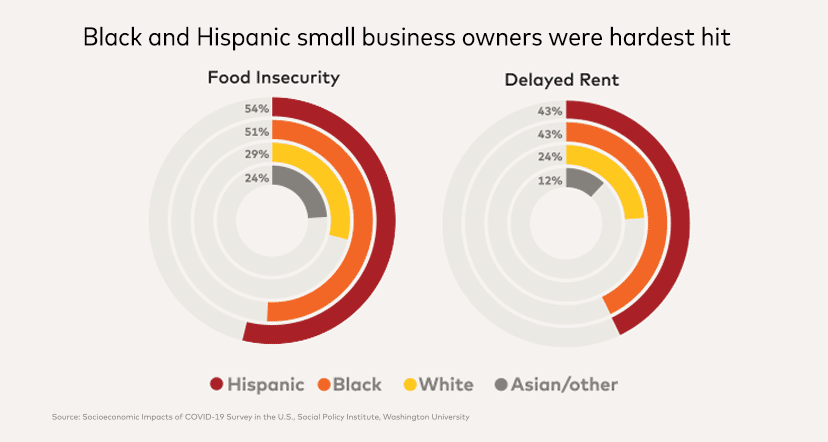

The worst hit by this economic upheaval were Black and Hispanic entrepreneurs. Lost in the success stories of large companies that survived or even thrived because of the infusion of some short-term funds from the CARES Act or banks was a more challenging reality: the study documents how the majority of small business owners instead turned to friends and family, and Black and Hispanic entrepreneurs were particularly reliant on their networks with 62 and 67 percent respectively saying they relied on friends and family for support, compared to 49 percent of white entrepreneurs.

Though Black and Hispanic entrepreneurs commonly reported access loans from government or financial institutions, these sources did not appear sufficient to keep them from turning to their friends and family for support as well. In turning to those closest to them, business owners placed further strain on personal networks that in many cases were themselves already stretched. This use of personal savings or networks of friends and family may place entrepreneurs and their families in a precarious personal financial position that ultimately threatens the growth of their business.

There is reason to be concerned about the current and future economic hardship we are seeing in these historically vulnerable communities. While the direct hardships on these communities are well-known by now, in the coming months we will likely hear more about how entrepreneurs’ communities – who often had to step in to help entrepreneurs when government support was not enough – faced their own financial hardships in order to provide these lifelines.

Small business owners, especially minority-owned entrepreneurs, need and deserve a better and trusted solution, and we must have programs in place before the next economic storm hits. Our research indicates that several key features are critical to include in this kind of government assistance.

First, money has to move faster and easier through trusted channels. Digitizing the application and distribution of funding by Community Development Financial Institutions (CDFIs) and minority depository institutions (MDIs), frontline financial institutions, will speed up the process. These systems need to be set up and integrated into other programs now, which will avoid much of the confusion and disconnects that delayed assistance during this crisis.

Second, we must improve the financial strength of small enterprises, notably minority-owned firms, before the next crisis strikes. A report by the Federal Reserve Bank of Atlanta showed that a majority of Black business owners used their personal credit, rather than their businesses’ credit, for financing. The situation worsens when they get denied loans or lack access to traditional financial services, opening the door for risky, high-cost alternatives, such as payday loans and check-cashing facilities. Alternatively, we ought to create safe alternative credit scoring and lending models that prioritize historically excluded entrepreneurs to help ensure greater wealth-building and financial stability.

Lastly, we might consider a benefits system that supports everyone, including the smallest businesses. Benefits should be designed and delivered with recipients at the center of the process. We must build on the progress of including the self-employed in the CARES Act as a way to reduce the risk of owning a small business, particularly for vulnerable populations. We should build a modern system of support that is portable, people-centered, and interoperable for small business owners, as well as their employees, as was outlined in a report by the Aspen Institute.

The pandemic showed all of us just how precarious is the financial position of many small businesses. It exacerbated many of society’s existing economic inequities. Now is the moment to address the systematic changes that are necessary to ensure America’s entrepreneurs are ready and more resilient ahead of the next storm.

As we do this, we need to take a far closer and more careful look at the unique situation and challenges of Black and Hispanic business owners and ensure that more equitable, accessible and trusted supports are in place. Because if we fail to strengthen these small businesses, the bottom will fall out for all businesses. If we don’t provide more equitable access to financing, inequality will only grow. And if we don’t adequately prepare these entrepreneurs for the next crisis, it may well be their last.

Michal Grinstein-Weiss is Director of the Social Policy Institute at Washington University in St. Louis and Salah Goss is Senior Vice President, Social Impact, Mastercard Center for Inclusive Growth

To view the original article, click here.

Check out more content from the Mastercard Center for Inclusive Growth